Can You Get Approved for Home Loans For Bad Credit in Illinois?

Yes! Even with a low credit score, you can still qualify for home loans for bad credit in Illinois. Many people in Chicago, Naperville, Aurora, Joliet, Rockford, and throughout Illinois assume poor credit automatically disqualifies them from buying a home. That is not the case.

Lenders like Capital Lending Network specialize in helping borrowers who have been turned away by traditional banks. Whether you’ve had bankruptcy, foreclosure, judgments, or collections, there are mortgage programs designed specifically for borrowers seeking home loans for bad credit.

This comprehensive 2025 guide will walk you through every step to getting approved, including Illinois-specific loan programs, tips for self-employed borrowers, and the most flexible loan options available today.

Step 1: Check Your Credit Before Applying for Illinois Home Loans For Bad Credit

Your credit score is the foundation of mortgage approval. Lenders in Illinois review it to determine how risky it is to provide you a loan.

Here’s how different loan types handle credit scores for Illinois borrowers:

- FHA Loans Illinois: Minimum 500 for 10% down, 580+ for 3.5% down

- VA Loans Illinois: No minimum score required; most lenders prefer 580+

- USDA Loans Illinois: 640+ recommended for automated approval; manual underwriting possible

- Conventional Loans Illinois: 620+ minimum

- Non-QM Loans Chicago & Suburbs: Flexible, no strict minimum; ideal for self-employed borrowers

Tip: Check your credit report for errors. Correcting even a single mistake can improve your score enough to qualify for better home loans for bad credit in Illinois.

For more guidance, visit the Consumer Financial Protection Bureau at https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/.

Step 2: Improve Your Credit Score to Qualify for Home Loans For Bad Credit

If your credit score is below 580, consider improving it before applying to increase your chances of approval. Illinois borrowers often take these steps:

- Pay down credit card balances, keeping utilization below 30%

- Make every payment on time; late payments significantly lower your score

- Avoid new debt; don’t open new credit cards or loans before applying

- Add positive credit with secured credit cards or credit-builder loans

Some lenders, like Capital Lending Network, offer rapid rescore services that can adjust your credit score quickly, giving you a better chance to qualify for home loans for bad credit in Chicago and surrounding areas.

Step 3: Gather Documents Needed for Home Loans For Bad Credit in Illinois

To prove your ability to repay, lenders require documentation. Prepare the following:

- Last 2 years of tax returns (unless using bank statement loans)

- W-2s or 1099s (for self-employed borrowers)

- Recent pay stubs (last 30 days)

- Bank statements (last 2 months)

- Proof of down payment funds

- List of debts and monthly obligations

Tip: Self-employed borrowers in Illinois can qualify using bank statement loans instead of tax returns, which simplifies the process and opens doors to more flexible financing.

Step 4: Get Pre-Approved for Home Loans For Bad Credit in Illinois

Getting pre-approved helps you understand your price range and strengthens your offer in competitive Illinois housing markets like Chicago, Aurora, Naperville, and Joliet.

During pre-approval, lenders will:

- Check your credit score

- Review income and debts

- Estimate your loan amount and interest rate

With Capital Lending Network, pre-approvals are fast, flexible, and designed for Illinois borrowers who need home loans for bad credit, even with recent credit challenges.

Step 5: Choose the Right Home Loan Program in Illinois

Even with bad credit, Illinois borrowers have multiple options:

- FHA Loans: Ideal for first-time homebuyers; allows scores as low as 500 with 10% down or 580+ with 3.5% down. Higher debt-to-income ratios accepted. Open collections and charge-offs may be approved with AUS approval.

- VA Loans: No minimum credit score, $0 down, no PMI, and flexible with debt-to-income ratio. Perfect for veterans and active military members in Illinois.

- Non-QM Loans: Great for self-employed borrowers or those with recent credit issues. No waiting period after bankruptcy, foreclosure, or short sale. Bank statement loans allowed, and debt-to-income ratios up to 55% accepted.

- Conventional Loans: Require minimum 620 credit score, lower rates for higher scores, PMI required if putting less than 20% down, and a 3% down option for first-time buyers.

For Illinois-specific assistance programs, see the Illinois Housing Development Authority at https://www.ihda.org/ for down payment help and grants.

Step 6: Mortgage Underwriting for Illinois Bad Credit Borrowers

Underwriting is the lender’s review of your financial situation. Lenders in Illinois will check:

- Credit history: late payments, collections, past bankruptcies

- Income and employment: stable job history and consistent income

- Debt-to-income ratio (DTI): monthly debts compared to income

- Assets: savings, investments, and reserves

Approval here means you’re close to closing on your Illinois home loan for bad credit.

Step 7: Closing On Your Home Loan in Illinois

At closing, Illinois borrowers will:

- Review and sign mortgage documents

- Pay closing costs (unless waived or rolled into the loan)

- Receive the keys to their new home

Closing marks the final step to securing home loans for bad credit in Illinois, including Chicago and surrounding suburbs.

Unique 2025 Insights About Home Loans For Bad Credit in Illinois

Here are insights you won’t find elsewhere:

- AI-Powered Underwriting: Many Illinois lenders now consider non-traditional data like rent and utility payments to approve borrowers with limited credit histories.

- Second-Chance Loan Programs: Illinois offers niche programs allowing buyers to qualify as early as 3 months after bankruptcy.

- Digital Bank Statement Loans: Self-employed borrowers in Chicago can link accounts digitally to verify income instead of providing tax returns.

- Rental History Reporting: On-time rent payments are increasingly being used to boost credit scores for mortgage approval.

- Down Payment Assistance Updates 2025: IHDA and local programs provide grants that do not require repayment, perfect for first-time homebuyers with low cash reserves.

For Illinois housing market data, see Illinois Realtors Market Stats at https://www.illinoisrealtors.org/marketstats/.

Why Choose Capital Lending Network for Illinois Home Loans For Bad Credit

Unlike national banks, Capital Lending Network specializes in Illinois borrowers with:

- Credit scores as low as 500

- High DTI ratios (up to 55%)

- Recent bankruptcies or foreclosures

- Bank statement loans for self-employed Chicago-area borrowers

Whether you’re searching for home loans for bad credit in Chicago, Naperville, Aurora, Joliet, or Rockford, CLN provides programs other lenders won’t.

FAQs About Home Loans For Bad Credit in Illinois

Q: Can I get approved with a credit score under 600 in Chicago?

A: Yes, FHA loans allow scores as low as 500, while VA and Non-QM loans offer flexible alternatives.

Q: What’s the easiest Illinois home loan for bad credit?

A: FHA loans are typically the most forgiving, especially for first-time homebuyers.

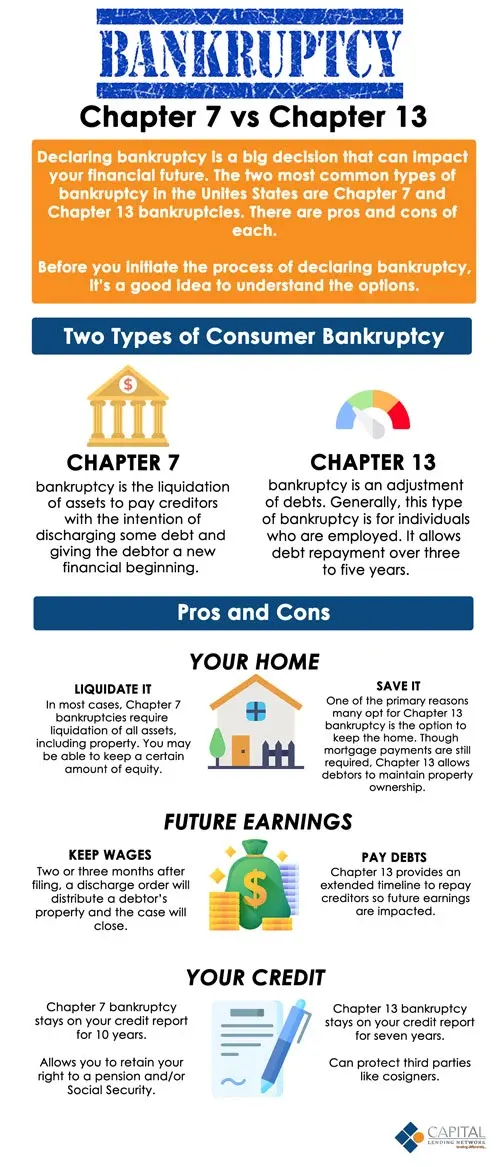

Q: Can I get a mortgage after bankruptcy or foreclosure in Illinois?

A: Yes. FHA requires 2 years after Chapter 7 bankruptcy, but Non-QM loans may allow no waiting period.

Q: What documents do Illinois lenders require?

A: Tax returns, W-2s/1099s, recent pay stubs, bank statements, proof of down payment, and debt records.

Q: Are there programs for first-time Illinois buyers with bad credit?

A: Yes. IHDA and local programs offer grants and forgivable loans for down payments and closing costs.

Final Thoughts

Whether you live in Chicago, Aurora, Naperville, Joliet, or Rockford, getting approved for home loans for bad credit in Illinois is possible in 2025. By following these steps:

- Check and improve your credit

- Gather all required documents

- Get pre-approved

- Choose the right loan program

- Work with Capital Lending Network

You can become a homeowner even with past credit challenges.

For practical budgeting and homeownership prep, visit Smart About Money at https://www.smartaboutmoney.org/.

{kind=link}